How to Assess Your Fundraising Readiness Before Approaching Investors

Jun 18

•

16

min read

Fundraising strategy

Saurabh Lahoti

Saurabh Lahoti is the founder of GTMDialogues, helping early-stage B2B startups scale with sharper GTM strategy, inbound marketing, and founder-led storytelling.

Founders spend weeks perfecting their deck before they start raising. But very few spend time researching the right investors, the right stage, with the right proof points.

Part 1 of this series covered the investor's world, how a VC fund works, what drives their decisions, and where your edge as a founder actually sits.

This article is about your side of the table discussing where you as a founder stand, what you need to prove, and how to make sure the investor you are walking into is actually the right one for where you are today.

How to Find the Right Investor for the Right Capital

When Zepto raised its first round in 2021, it went to angels and early-stage investors willing to back a ten-minute grocery delivery thesis before anyone had proven the model worked at scale. Two years later, when it raised at a billion-dollar valuation, it went to a completely different set of investors with a completely different set of expectations.

Same company. Same founders. Different capital. Different conversation.

Marc Andreessen of Andreessen Horowitz has put the math plainly: of roughly 4,000 venture-fundable companies in any given year, about 200 get funded by a top-tier VC, and of those, only 15 will ever reach $100 million in revenue. Those 15 generate roughly 97% of all returns for the entire category.

That is the world every investor is operating in when they sit across from you. The question is whether you understand which part of that world you are in right now

Know Where Your Startup is Placed in Fundraising Spectrum

Think of the funding landscape as a spectrum of risk appetite and return expectation, with each investor type optimising for something fundamentally different.

At one end sit angel investors. They are individuals deploying their own capital at pre-seed or idea stage, with check sizes ranging from a few lakhs to a few crores in India and $25,000 to $100,000 in most global markets. They back on conviction, relationship, and a personal belief in the founder.

Rajan Anandan of Peak XV Partners, who has made over 80 personal angel investments across India and Southeast Asia, has described this moment as backing founders when conviction matters more than metrics. That is the contract an angel is signing. They are betting on you before the numbers exist.

Seed funds operate with a different mandate entirely. They are institutional, they deploy pooled capital, and they need the math to work across a portfolio of bets. According to Kruze Consulting's analysis of VC return expectations, seed investors shoot for 100x returns on individual investments, knowing that most will fail and a small number of outliers will carry the fund. A seed fund writing a check into your company is not hoping you do well. They are hoping you become the one company that makes everything else worth it.

Series A investors operate with a more refined lens. By this stage the return expectation drops to 10 to 15x, but the bar for what constitutes evidence rises significantly. They want to see a repeatable sales motion, retention signals, and a clear path to the kind of scale that justifies their check size. The bet shifts from the founder to the model.

Growth funds at Series B and beyond are buying scale, not potential. Their return targets sit at 3 to 5x, which sounds conservative until you realise the check sizes are large enough that 3x still represents hundreds of millions of dollars returned. They are not taking bets on unproven models. They are accelerating businesses that have already figured out the engine and just need more fuel.

Why the Same Startup Needs a Different Investor at Every Stage

Vinod Khosla has pointed out that many investors tend to overweight revenue and underweight asset building, which means if your business is building something whose value is not yet visible in a revenue line, such as network effects, proprietary data, or deep-tech foundations, you need to find the investors who have the framework to see it. Pitching a revenue-first fund on a network-effect thesis is a structural mismatch. It is not a pitch problem, no amount of slide improvement fixes it.

How Airbnb's Rejections Prove That Fund Timing Matters as Much as the Idea

In 2006, when Brian Chesky and Joe Gebbia were pitching Airbnb, they were turned down by seven of the top Silicon Valley firms. The idea was not the problem. The stage was not the problem. Several of the funds they approached had either recently backed a competitor in the space or were in the later years of a fund cycle where writing new early-stage checks had become complicated. The founders who eventually said yes were the ones whose fund structure and timing made the bet logical. The others were not wrong about Airbnb. They were misaligned with it at that moment.

Time Your Pitch to the Fund's Cycle and Timelines

Fred Wilson of Union Square Ventures, whose portfolio includes Twitter, Etsy, and Coinbase, has written about something most founders never consider: venture funds operate on a seven to ten year clock, and where a fund sits on that clock changes everything about how urgently they need to write new checks.

A fund in year two is actively deploying capital. The partners are hungry to find new companies, build the portfolio, and put their LP commitments to work. They have time, flexibility, and a mandate to move. A fund in year seven or eight is in a completely different position. They are managing existing companies toward exits, not hunting for new bets. The checks they write at this stage tend to be follow-ons into existing portfolio companies rather than new investments.

When you approach a fund without knowing where they sit on that clock, you are essentially showing up to a dinner party at the wrong time. The food might be excellent. The timing just does not work.

Three Things to Know About a Fund Before You Send a Single Email

The first thing to understand is the fund's recent portfolio activity. Thesis alignment requires looking at what a fund has backed in the last 18 months, not their historical portfolio. A fund that backed three fintech companies in the last year and has no exits yet is unlikely to write a fourth fintech check.

A fund that has been quiet in a sector for two years may be actively looking to re-enter it. The recent deals tell you more about where a fund is headed than their stated thesis ever will.

The second thing to understand is check size relative to your round. A fund that writes $500,000 checks cannot lead a $3 million seed round even if the partner loves your startup. Their economics simply do not work. This is not a rejection. It is a structural mismatch that has nothing to do with your business.

The third thing to understand is which partner is actively looking for new investments in your space. Most funds have partners with different focus areas and different energy levels toward new deals. A warm introduction to the right partner inside a fund that is theoretically a fit is worth more than a cold approach to the right fund with the wrong partner.

Lightspeed India, Blume Ventures, and Peak XV all have publicly available portfolio pages, partner profiles, and in many cases published investment theses. The founders who do the work to understand each fund's current posture before they reach out consistently move faster through the funnel than those who treat every fund as a single undifferentiated target.

Before you send a cold email or ask for an introduction, these three questions need clear answers.

Where is this fund in its deployment cycle? Year two and year seven are different conversations. The fund's vintage year is usually publicly available through Crunchbase or their own announcements.

Has this fund recently backed a direct competitor in my space? If yes, they are unlikely to back you. If they backed an adjacent company that failed, they may be more interested than their public posture suggests.

Which specific partner at this fund has the clearest thesis overlap with what I am building? A fund-level fit means nothing without a partner-level champion inside the firm to push the deal through the partnership.

Why Jim Goetz Backed WhatsApp on a Beachhead, Not a TAM Slide

In 2011, when Jim Goetz of Sequoia Capital wrote an $8 million check into WhatsApp, the messaging market was already crowded. BlackBerry Messenger had millions of users. SMS was ubiquitous. By any traditional market sizing framework, the TAM for messaging was enormous but so was the competition. Goetz was not betting on the TAM slide. He was betting on a specific beachhead: users who wanted cross-platform messaging without paying per-SMS charges, in a world where smartphones were just beginning to replace feature phones. That beachhead turned into 450 million users, and Sequoia's investment returned roughly 50 times when Facebook acquired WhatsApp for $19 billion in 2014.

Goetz has since made his view on market sizing explicit. Speaking publicly on the subject, he has said: "There's no TAM, there's no SAM, only early beachhead customers."

A $100 Billion Market Claim Means Nothing Without a Specific Entry Point

A VC who has sat through two hundred pitches has seen the same $100 billion market claim presented by thirty different founders in the same sector. The number itself carries no information. What carries information is the specific path through that market, the beachhead the founder is entering first, why that segment has acute pain, and how dominance in that segment creates the leverage to expand into the broader opportunity.

Don Valentine built Sequoia's entire philosophy around this distinction. His checklist required a very big market, not because a large TAM number was impressive, but because the market had to be big enough to allow the company to become significant even if it only captured a fraction of it. The market size mattered because of what it enabled, not because of what it looked like on a slide.

How to Build a Market Argument From the Beachhead Out, Not the TAM Down

A compelling market argument has four components that work together as a single coherent thesis. Most founders present them as four separate slides. The ones who raise well present them as one connected story.

i) The beachhead: The specific, narrow segment you are entering first. Small enough to dominate, large enough to sustain the business. This is the segment where your product-market fit is strongest, your unfair advantage is most visible, and word of mouth can spread before you need to expand. If you cannot name it in one sentence, it is not specific enough.

ii) The growth path: From the beachhead, how does the company expand? What adjacent segments open up once you have won the first one? This should be grounded in what you already know about your customers' adjacent problems, not a speculative land-grab on a slide.

iii) The timing argument: Why is this beachhead available right now? What has changed in regulation, technology, infrastructure, or customer behaviour that has created this opening? A beachhead that existed five years ago and nobody captured is a red flag. A beachhead that has just opened because of a specific shift is a now-or-never case.

iv) The size of the prize: Not the total addressable market as a static number, but a credible calculation of what the revenue opportunity looks like if you win the beachhead and expand one or two steps along the growth path. This is the number that belongs on the slide, not the total market.

When Freshworks was building its early market case, it led with a specific problem: small and mid-market businesses being priced out of enterprise software like Salesforce and underserved by tools too complex to implement without an IT team. That beachhead was specific, urgent, and large enough to build a business on. Freshworks went public on Nasdaq in 2021 at a valuation of over $10 billion. The market argument held up because it started with a real entry point, not an abstraction.

The One Question to Answer Before You Build Your Market Size Slide

Before you build a market size slide, answer this question honestly: if you could only serve one narrow segment of customers for the next 18 months, which segment would give you the clearest path to becoming the undisputed leader in that space?

That segment is your beachhead. Build the market argument outward from there. A VC who understands exactly where you are starting, why that segment is available now, and how winning it opens the door to a much larger opportunity will always find that more compelling than a circle diagram with a large number inside it.

How to Show a VC That Passing Means Watching Someone Else Take the Window

There is a version of urgency that VCs see constantly and discount immediately. It is manufactured scarcity: "we are closing the round in three weeks," "two other term sheets are coming," "this is a limited window." These create transactional pressure but they do not answer the timing question. They are tactics, not arguments.

The urgency that actually moves a VC is structural, not transactional. It comes from demonstrating that specific conditions, regulatory, technological, behavioural, or infrastructural, have converged right now in a way that creates a window for your startup to win. A window that was not open before and will not stay open indefinitely.

The test is simple. If a VC can look at your business and think "I can come back to this in 18 months when the risk is lower and the thesis will be equally valid," you have not made a now-or-never case. You have made a wait-and-see case. Those rarely get funded.

The Three Components of a Timing Argument to Keep Investors Interested

A credible timing argument is built from evidence, not assertion. It has three specific components that together make waiting feel like a mistake.

i) The shift: Name the specific thing that has changed. Not "AI is transforming everything" or "customers are moving to digital." The specific regulation that passed, the specific infrastructure that became available, the specific behaviour shift that is measurable and recent. When the Account Aggregator framework went live in India in 2021, it created a specific, verifiable shift in what was possible for fintech and lending startups. Founders who could name that shift and connect it directly to their product had a timing argument. Founders who said "fintech is growing" did not.

ii) The window: Show why this shift creates a window that is open now and will close. Markets that shift attract entrants. The early movers take the ground before distribution channels get crowded, before incumbents respond, and before the cost of customer acquisition rises. The window is real because incumbents are slow, not because the opportunity is permanent. A VC needs to feel that backing you now is participating in the early part of that window, and passing means watching someone else take it.

iii) The cost of waiting: This is the part most founders leave out entirely. What specifically happens to this opportunity if no one moves on it in the next 12 months? Does a larger incumbent enter? Does the regulatory window close? Does the customer behaviour shift become table stakes rather than an edge? A timing argument without a cost of waiting is incomplete. The urgency only lands when the VC can see what the world looks like if they pass and someone else does not.

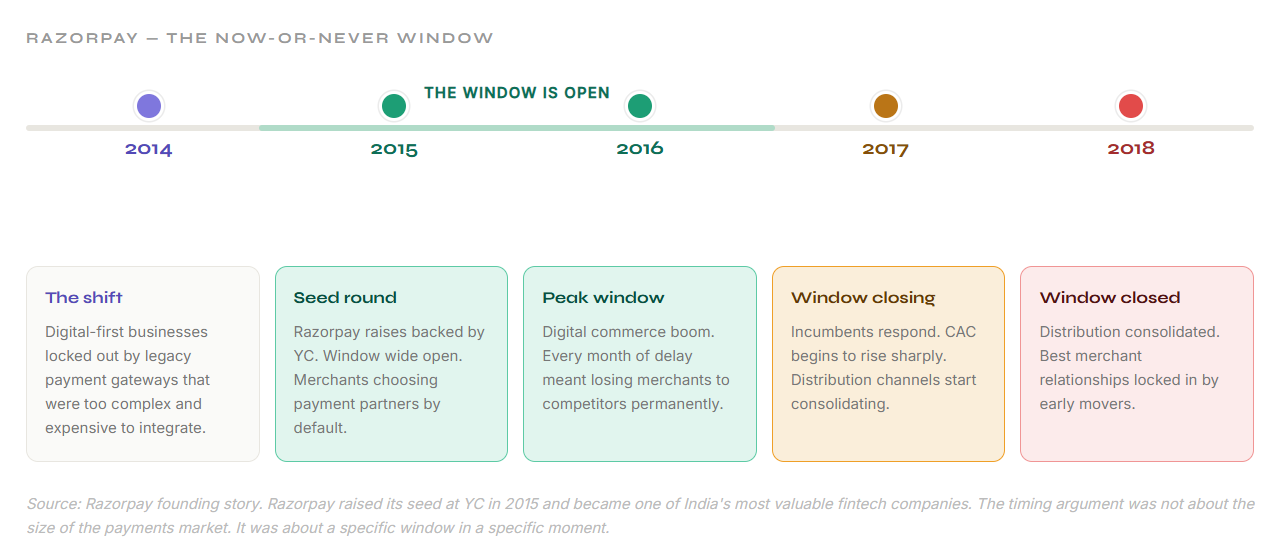

When Razorpay was building its case in 2014, the timing argument was precise. The shift was India's growing base of digital-first businesses that needed payment infrastructure but were locked out by the complexity and cost of legacy payment gateways.

The window was the early years of the digital commerce boom before larger players consolidated distribution. The cost of waiting was that every month of delay meant more merchants choosing a competitor by default. Razorpay raised its seed round in 2015 and went on to become one of India's most valuable fintech companies. The timing argument was not about the size of the payments market. It was about a specific window in a specific moment.

Before you pitch your timing argument, answer this honestly: if someone else builds exactly what you are building but starts 18 months from now, do they miss the window entirely or do they simply start later?

If the answer is "they simply start later," you do not have a now-or-never case. Go back and find the specific structural reason why the window closes.

If the answer is "they miss it," you have the core of your timing argument. Build the evidence around that.

Band Muthi Lakh Ki: Every Stage Has Its Own Language and Investors Are Fluent in All of Them

There is an old saying in Indian business circles: ‘band muthi lakh ki, khuli to khaak ki’. A closed fist is worth a lakh, and an open one is worth nothing. The point is not about secrecy. It is about knowing what you have, protecting it, and deploying it at the right moment.

In fundraising, the equivalent truth is this: every stage has a specific set of metrics that signal readiness, and showing up with the wrong metrics at the wrong stage is the equivalent of opening your fist too early.

Paul Graham of Y Combinator framed this as a single binary question he asks every founder he meets: "Is your startup default alive or default dead?" A startup is default alive if it can reach profitability before it runs out of money without raising another round. Default dead means it cannot.

Graham's point is not that every startup should be profitable. It is that every founder should know exactly where they stand, because an investor will know within minutes of looking at your numbers.

That question means different things at different stages. Here is what it translates to in practice:-

i) Pre-seed: The investor is betting on you, not your numbers

At pre-seed, there are rarely numbers worth betting on. What a pre-seed investor is underwriting is the founder's proximity to the problem, the sharpness of the insight, and the credibility of the market thesis. The signals that matter at this stage are qualitative: letters of intent from potential customers, a waitlist that suggests real demand, early conversations that surface a specific pain no existing solution addresses.

ii) Seed: The investor is betting on early evidence of product-market fit

By the time you are raising a seed round, qualitative signals are not enough. A seed investor needs to see that customers exist, that they are paying or actively using the product, and that there are early signals of retention.

According to Forum Ventures' 2024 State of Seed report, the benchmark has shifted meaningfully: $300,000 to $500,000 in ARR is now the standard expectation at seed stage, up from approximately $200,000 in 2023.

Retention is the metric that separates real traction from vanity metrics at this stage. A company growing 15% month on month with 10% monthly churn is a leaking bucket. The growth looks impressive until an investor builds the cohort model. Month on month growth of 10 to 15% with strong retention is the language a seed investor wants to hear.

iii) Series A: The investor is betting on a repeatable engine

Series A is where the conversation shifts from product-market fit to business model. An investor at this stage wants to know that you have figured out how to acquire customers predictably, retain them, and expand revenue within the existing base. The benchmarks are specific.

According to Carta data cited by spectup, the median Series A company in 2025 had $1.5 million in ARR. Investors expect two to three times year on year growth, net revenue retention above 110%, CAC payback under 12 months, and a burn multiple below 1.5x.

iv) Series B and beyond: The investor is betting on market leadership

By Series B, the question is no longer whether the business works. It is whether you can become the dominant player in your market. The metrics at this stage are about market expansion, operating leverage, and a credible path to profitability.

Distribution has consolidated, the beachhead has been won, and the investor is asking whether the company can defend and expand its position before a larger player or a better-funded competitor shows up.

Before You Raise, Ask If Your Metrics Match the Round You're Actually Ready For

Before you go out to raise, build a one-page view of your metrics and ask one question: do these metrics tell the story of a company that is ready for the round I am raising, or the round before it? Most founders who struggle to raise are not raising the wrong amount.

They are raising at the wrong stage for the signals they have. The language of each stage is different. Speaking the wrong one does not just confuse the investor. It tells them you do not know where you are.

The founders who raise well are not the ones with the best decks. They are the ones who have done this work before anyone else sees the pitch. That work is what this article is about.

Frequently Asked Questions

How do I know which type of investor is right for my startup right now?

The answer sits in your current stage and the signals you have. If you have a thesis and early customer conversations but no revenue, an angel is the right first call. If you have $300,000 to $500,000 in ARR with early retention signals, a seed fund makes sense. If you have a repeatable sales motion and $1.5 million or more in ARR, you are ready for a Series A conversation.

How do I find out what stage of its fund cycle a VC is in?

A fund's vintage year is usually publicly available. Check the fund's announcement on their website, their Crunchbase profile, or press coverage from when the fund closed. A fund that closed in 2022 and has been actively investing is likely in years three to four of its cycle, which means it is still deploying but becoming more selective. A fund that closed in 2018 is likely in harvest mode and writing very few new checks outside its existing portfolio.

What is the difference between TAM and a beachhead market?

TAM is the total size of the market you could theoretically address if you captured every customer. A beachhead is the specific, narrow segment you are entering first. The beachhead is small enough to dominate but large enough to sustain the business. Jim Goetz of Sequoia has put it directly: there is no TAM, there is no SAM, only early beachhead customers. A credible market argument starts with the beachhead and builds outward, not the other way around.

How do I make a timing argument without it sounding like manufactured urgency?

Manufactured urgency is transactional: closing the round in three weeks, two other term sheets coming. Real urgency is structural: a specific regulation, infrastructure shift, or behaviour change that has created a window that did not exist before and will not stay open indefinitely. The test is simple. If someone builds exactly what you are building 18 months from now, do they miss the window entirely or do they simply start later? If the answer is to miss it entirely, you have a real timing argument. Build the evidence around that.

What is net revenue retention and why do Series A investors care so much about it?

Net revenue retention measures how much revenue you retain and expand from your existing customer base over a period, typically 12 months. An NRR above 100% means your existing customers are spending more than they were a year ago. An NRR above 110% is the benchmark most Series A investors look for because it tells them the product is worth keeping, expanding, and ultimately worth investing in at scale. Many Series A investors treat NRR below 100% as a signal of a fundamental product-market fit problem that no amount of new customer growth can mask.

Should I approach multiple investors at different stages at the same time?

Only if they are genuinely appropriate for your current stage and signals. Running a parallel process is standard and expected. What kills rounds is approaching investors at the wrong stage simultaneously, where a seed fund and a Series A fund both pass for different reasons and neither conversation generates momentum for the other. Build your target list by stage first, then run the parallel process within the right tier. A well-structured process within the right investor type creates urgency. A scattered process across the wrong types creates confusion.

Saurabh Lahoti

Saurabh Lahoti is the founder of GTMDialogues, helping early-stage B2B startups scale with sharper GTM strategy, inbound marketing, and founder-led storytelling.

.png)

.png)

.png)

.png)